Preparing For KLAC and Learning About The Industry

$KLAC is currently around fair value, but I figured the research is still worth it...

Introduction:

I really want to learn more about the semiconductor industry so I decided I wanted to go over some of the companies within the industry to get to know it better. KLA is a company that I think is probably on the fair value - slightly overvalued territory, but as we have seen over the last few years, the market can become irrational with the pricing. This company is going to go onto my watchlist and I will make an update if it ends up falling. In the meantime, enjoy the write-up and let me know if you have any other ideas or want to see a certain company from the semis be talked about. Unfortunately, I had the opportunity to start buying at $250 - $260 but didn’t feel like I knew the business enough so I held off. Obviously, in short-term hindsight, I do not feel good about not buying, but I don’t think I would have that same regret if the price would have kept going down. It is all about managing my own emotion and knowledge in the end.

If you would like to watch my Youtube video explanation click here.

Disclaimer: I currently do not have a position in this company.

KLAC - KLA Corporation:

“KLA Corporation and its majority-owned subsidiaries (“KLA” or the “Company” and also referred to as “we,” “our,” “us,” or similar references) is a supplier of industry leading equipment and services that enables innovation throughout the electronics industry. We provide advanced process control and process-enabling solutions for manufacturing wafers, reticles, chemicals/materials, integrated circuits (“IC” or “chip”), packaged ICs, printed circuit boards (“PCB”), and flat panel displays (“FPD”), as well as comprehensive support and services across our installed base. Our suite of advanced products, coupled with our unique yield management software and services, allow us to deliver the solutions our customers need to achieve their productivity goals, including improving yields and reducing waste, by significantly reducing their risks and costs and improving their overall profitability and return on investment.” - 2022 10K Page 5

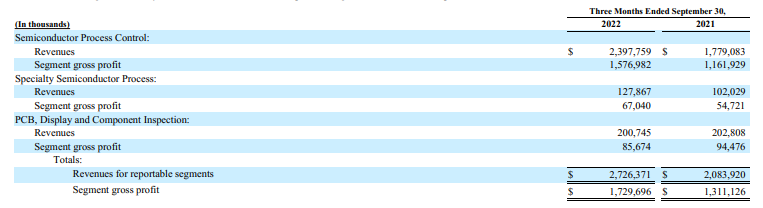

KLA Corporation breaks itself down into the following segments:

“Within the Semiconductor Process Control segment, our comprehensive portfolio of inspection, metrology and software products, and related services, help IC, wafer, reticle and chemical/materials manufacturers achieve target yields throughout the entire fabrication process, from R&D to final volume production. These products and services are designed to provide comprehensive solutions to help customers accelerate development and production ramp cycles, achieve higher and more stable product yields and improve their overall profitability.

Within the Specialty Semiconductor Process segment, which includes the SPTS business, KLA develops and sells advanced vacuum deposition and etching process tools, which are used by a broad range of specialty semiconductor customers, including manufacturers of microelectromechanical systems (“MEMS”), radio frequency (“RF”) communication semiconductors, and power semiconductors for automotive and industrial applications.

Within the PCB, Display and Component Inspection segment, which includes the PCB, FPD, Frontline and ICOS businesses, KLA enables electronic device manufacturers to inspect, test and measure PCBs, FPDs and packaged ICs to verify their quality, pattern the desired electronic circuitry on the relevant substrate and perform three-dimensional shaping of metalized circuits on multiple surfaces.” - 2022 10K Page 5

From the Q1 10Q:

From 2022 10K:

The Other segment is comprised of one operating segment. During the fourth quarter of fiscal 2020, we entered into an Asset Purchase Agreement to sell certain core assets of our non-strategic solar energy business, OLTS, which accounted for the majority of our Other reportable segment. The sale was completed in the first quarter of fiscal 2021 with an insignificant amount of proceeds. This business was engaged in the research, development and marketing of products for the deposition of thin film coating of various materials on crystalline silicon photovoltaic wafers for solar energy panels. Prior to July 1, 2022, we had a fourth segment, Other, but core assets were sold and there are no longer operations. - 2022 10K Page 32 - 33

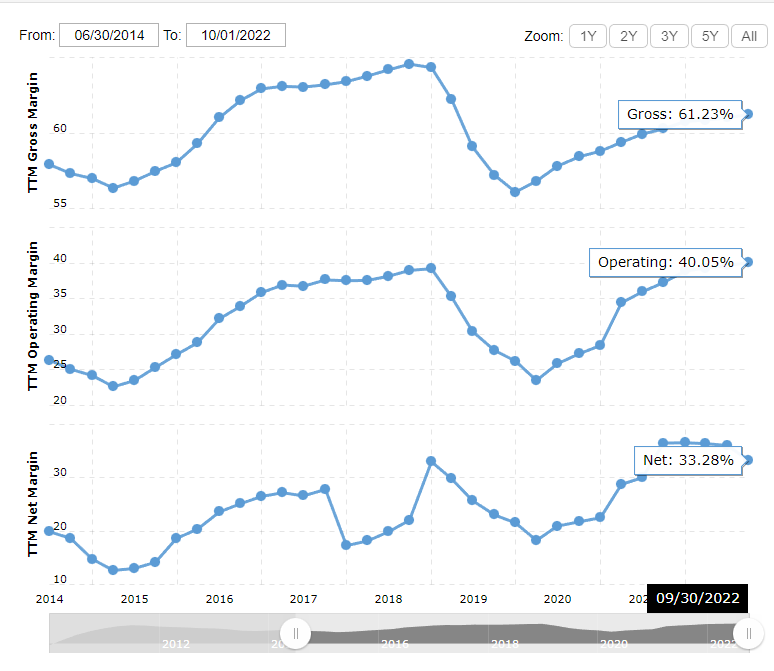

Financials:

Total Revenue TTM as of Q1 2023: $9.852B

Profit Margin has been floating between ~20% - 30% over the last few years

Current P/E: ~18.91

EV/EBITDA: ~14.39

Current Cash as of Q1 2023: $1.819B

Total Debt as of Q1 2023: $6.312B

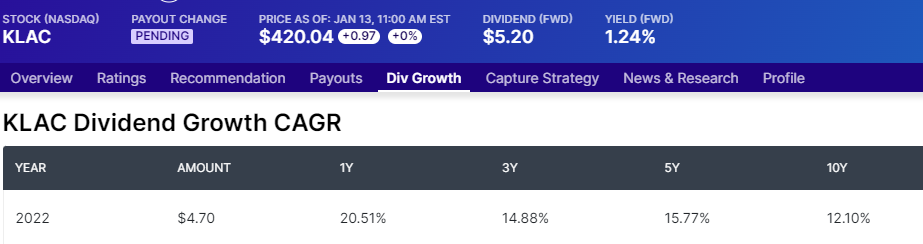

The company has been repurchasing shares and issuing dividends with large increases in the payout over the last few years. Their plan/goal is to pay out ~85% of their FCF to their shareholders. As of September 30, 2022, an aggregate of $3.14 billion was available for repurchase under the stock repurchase program. The below screenshot shows their ideal capital priorities and it comes from their June 2022 investor day presentation(link).

Industry

Process Control

The market for semiconductor manufacturing equipment is expected to grow in response to rising consumer electronics demand. The growing demand for semiconductor chips from producers of consumer electronics, medical gadgets, and sensor systems is driving the semiconductor industry forward. Expanding middle class, changing lifestyle preferences, and a growing desire to use smart electronic devices are among the key drivers driving consumer electronics growth in recent years. This indicates that the market for semiconductor manufacturing equipment would rise at a rapid pace over the forecast period.

However, tiny dust particles have an impact on the overall semiconductor manufacturing and fabrication process, which requires the use of a clean environment and clean equipment. Furthermore, production faults because of supply delays might result in extra losses in the form of order cancelation and client shifts to other suppliers. Because there are several patterns on a chip at such a small size, pattern complexity rises. This necessitates a high level of precision in order to convey accurate data to the chip. With the demand for size reduction and the high density of semiconductor devices, the complexity of wafers has increased, resulting in a drop in laser wavelength.

Furthermore, during the forecast period, the semiconductor industry is expected to grow at a CAGR of more than 5%. This is attributed to an increase in mobile and consumer electronic device sales. Over the forecast period, new technologies such as the Internet of Things (IoT), connected gadgets, ultra-high-definition (UHD) TVs, automotive automation, and hybrid laptops will continue to fuel demand for semiconductor processes and control equipment. This means that the industry will grow from $6.4B in 2020 to $10.24 by 2027. - MMR Research report

Strengths:

Capital Investment and MOAT

As seen in the screenshot above, they currently have over half the market share in the process control industry in terms of sales. KLA benefits from the upcycle in the semiconductor market because as more foundries and IDM factories are built out, the spent equipment and CAPEX grow larger and larger. Some of the largest companies like TSMC and Intel are investing heavily into their own infrastructure and KLA will benefit massively. The small document that KLA put together here, shows where KLA’s solution for process control fits into these manufacturers. Guaranteeing high yields is a necessity for these companies and KLA’s equipment help ensure that the semis have high yields.

Continuous Maintenance and Sustainment of Revenue

The customers of KLA seem to follow the “If it ain’t broke, don’t fix it” mantra because of the amount of older equipment still in operation today:

As KLA makes new products for leading-edge technology, the old equipment is still being used on the older nodes. This means that KLA gets to capture all of the revenue related to maintaining their products for their clientele. The companies buying these pieces of equipment are not interested in replacing them if it is still working within their processes to create semiconductors, wafers, and/or integrated circuits. As a key integral step in semiconductor manufacturing, process control allows the companies to have the best yield possible and reduce the cost per manufacturing cycle.

Weaknesses:

Foreign Revenue

Some companies are less exposed to political risk and the fact that sales are generated overseas in China isn’t as big of an issue. In KLA’s case, the majority of the sales are generated within China and Taiwan. While this may present opportunities for them to grow the NA segment of their geography(due to the recent investments in US plants), it can spell trouble in the near term if the US continues to pursue sanctions on China. The BIS instituted a restriction on advanced semi-tech going to China (link). As such, KLA added this to their most recent 10Q: “We are still assessing the aggregate potential impact of the existing regulations and New BIS Rules on our financial results and operations, although our preliminary assessment indicates a potential combined gross direct impact on revenue, based on existing backlog, in the range of approximately $500 million to $900 million in the calendar year 2023.” - Q1 2023 10Q Page 38

Continuous Research and Development

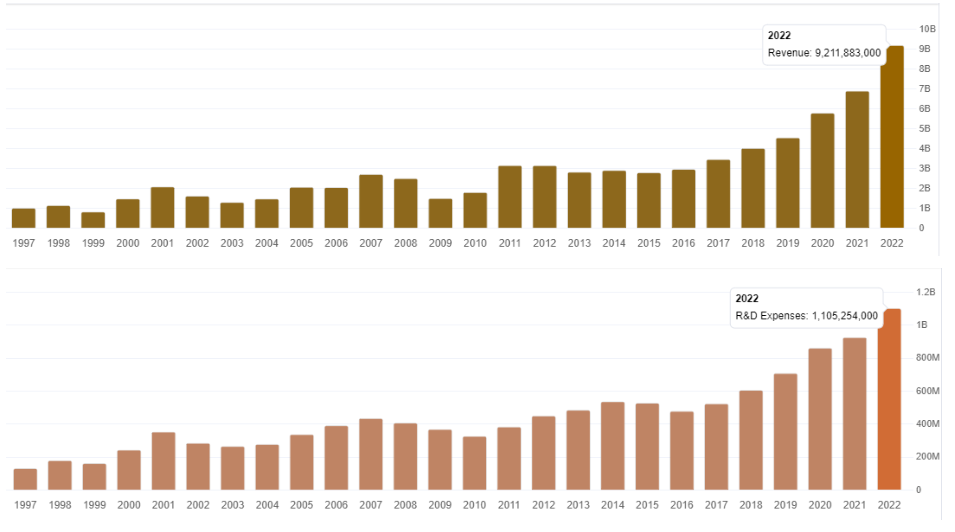

With a business model based on continuously keeping up with the new nodes that are reached, it is important to note the amount of R&D needed to bring process control to these smaller and smaller nodes. Part of the growth cycles in this cyclical industry means that it will ramp up R&D to stay current with its clients. As you can see here in the screenshots, the first one is the revenue annually and the second screenshot shows the R&D along with those sales. Unsurprisingly, you can see the cycles as they have gone up and down in both screenshots, but it is something I want to note since the complexity will keep increasing.

Debt

The last risk I want to mention is their debt and what they are doing with the free cash flow. While I think that using debt for capital allocation at low rates can be good if the company continues to generate returns above the interest rates. I do not think that paying out ~85% of your FCF is wise when they have so much debt on the balance sheet. As it stands today, their target range for Total Debt/ EBITDA is 1.5x to 2.0x and the current ratio as of Q1 2023 is 1.44. Increasing their debt consistently will be bad if the semiconductor industry enters a downturn. I would definitely keep an eye on this quarter to quarter. Ideally, I would like them to only lever up if they are adding to their manufacturing, making acquisitions, or adding to the growth of the company rather than trying to support their shareholders’ payouts (dividends or repurchases).

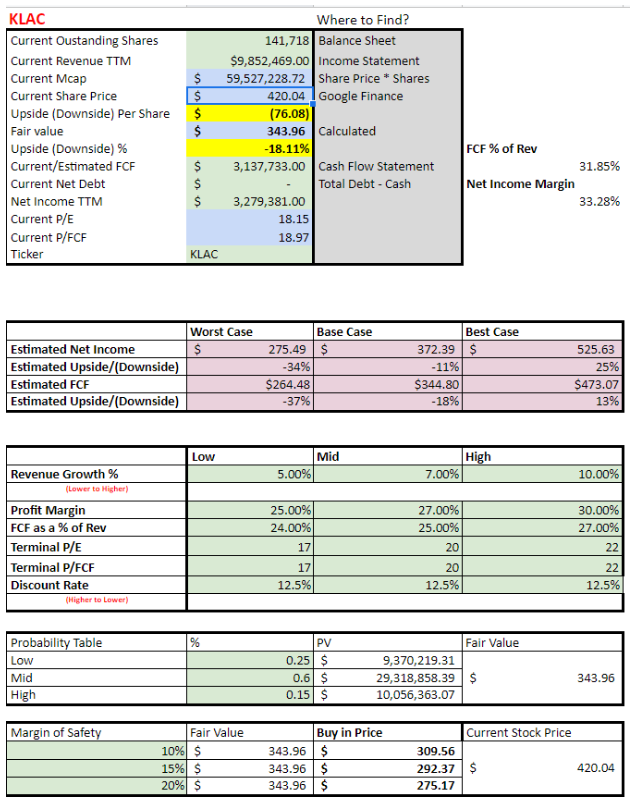

Intrinsic Value:

Link to discounted cash flow here.

Conclusion

I am waiting at today’s price, but given the cyclicality of this industry, I would not be surprised if it hit near its $250 52-Week Low again at some point over the next few years. I like the company at or around a $35B market cap, but I was not prepared when it dropped significantly a few months ago. Doing this write-up and research now will allow me to continue exploring and to make sure I am prepared during a downturn. I don’t see this research as a waste of time because this will allow me to better understand the industry as a whole and if I find an opportunity because of this research I will call that a win. I will keep you all posted if there are any developments.